What a 50-Year Mortgage Really Means for Homebuyers

The 50-year mortgage has been getting a lot of attention lately, especially as the federal government explores new ways to help younger buyers get into their first home. One idea being discussed is a government-backed 50-year fixed-rate mortgage. On the surface, it sounds like a solution to high monthly payments and rising affordability challenges, but the reality is far more complicated.

According to Mike Orr of the Cromford Report, a 50-year loan may stimulate demand, but it’s not a strategy he would recommend for first-time buyers. Because the payback period is so long, very little of the principal would be paid down in the first five years. That means a new homeowner would build almost no equity early on - often not enough to cover selling costs if life changes and they need to move. Any equity gains would rely heavily on home-price inflation. While that has worked in certain periods of strong appreciation, it would not have worked over the past three years.

There’s also the issue of long-term cost. A $350,000 mortgage on a standard 30-year loan today would typically create about $446,000 in interest payments over its life. Stretch that to 50 years and the interest jumps to about $833,000 - nearly double. And that’s assuming the 50-year mortgage comes with the same interest rate as a 30-year loan, which is unlikely. Based on current lender behavior, a 50-year loan would probably carry an extra 0.25 to 0.50 percent in rate.

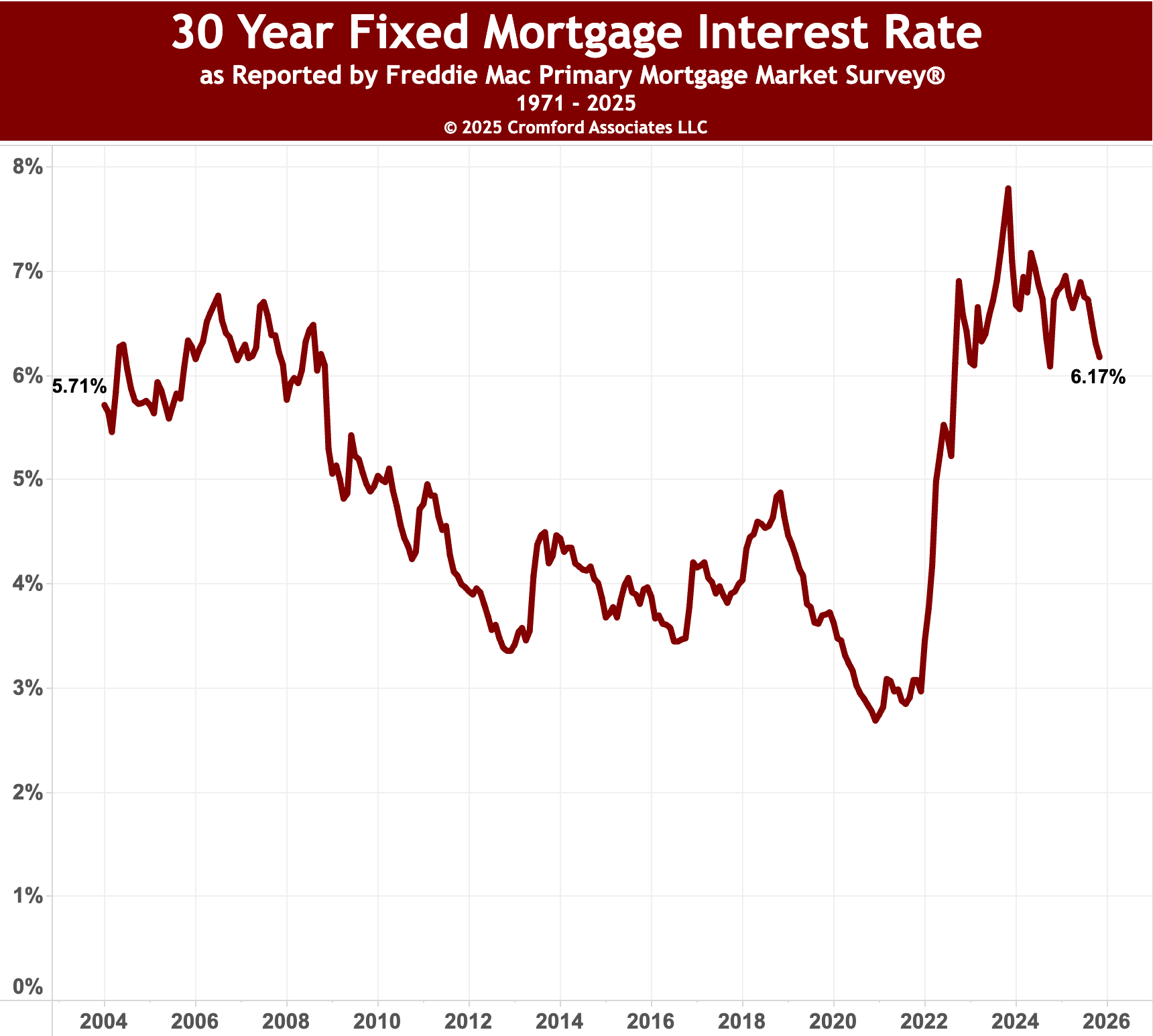

Here's a current (as of November 2025) 30 Year Fixed Mortgage Interest Rate reference for you.

While the appeal of a lower monthly payment is real - about $240 per month less on a $350,000 loan - the benefit is mostly an illusion. The lower payment comes almost entirely from reducing the amount of principal being paid each month. The interest portion actually grows. Orr compares principal repayment to putting money into a savings account: it increases your net worth. With a 30-year loan, that savings account is fully funded after three decades. With a 50-year loan, you haven’t even paid off half the principal until nearly year 40.

As discussions continue at the federal level, it’s important for buyers to look beyond monthly payment numbers and understand the long-term implications. Affordability solutions can be helpful, but not all of them build wealth - and some may do the opposite.